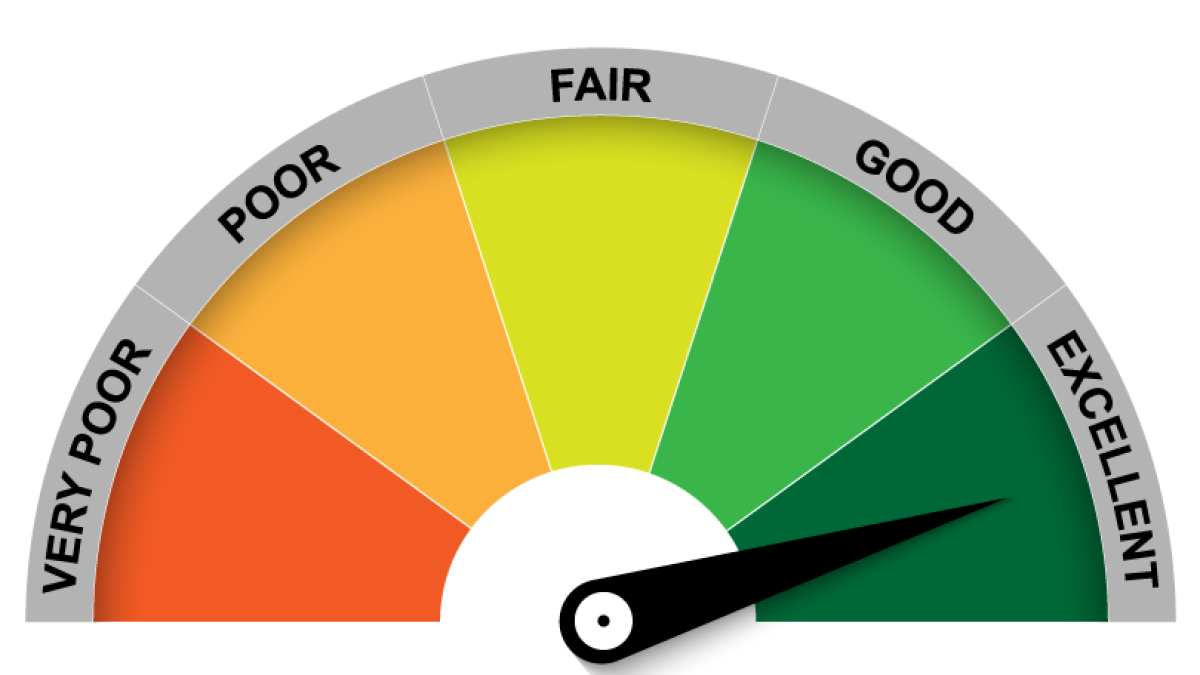

Hint: It’s Not Just Your FICO Score

Hint: It’s Not Just Your FICO Score

Whether you’re a startup seeking your first loan or a veteran looking to upgrade your equipment, you might wonder what lenders actually look for when deciding whether to approve your credit application.

Obviously, there’s your credit score. FICO and similar institutions determine your score by analyzing your debts owed, on-time payments, credit history and hard inquiries.

Most lenders, however, use more than just your FICO score to determine whether your business is creditworthy. They use other indicators of your financial health, such as your debt-to-income ratio to decide whether you’re approved for a loan.

Business Credit Score

In addition to your personal credit score, lenders also look at your business credit score to determine your eligibility. Business credit scores focus primarily on how you utilize your credit, how frequently you open new lines of credit and how quickly you pay off your debts.

Like your credit score, your business credit score provides a metric for lenders to evaluate your company’s creditworthiness. Ideally, you should have a business credit score of 75 or greater, but if your score is not ideal, you can often find loans at higher interest rates.

Payment History

Even if your overall credit score is less-than-perfect, having a solid payment history will help you attain financing for your major business equipment leases or purchases.

Lenders often focus on this portion of your credit report because it reflects whether you’re likely to make good on your debts. A record of on-time payments will work in your favor, but frequent missed payments and bankruptcies may tell lenders that you’re too high-risk.

Paying your bills on time is one of the easiest ways to improve your creditworthiness. It will boost your FICO score, showing lenders that your business is a safe bet.

Assets

To obtain financing, many businesses use their assets to take out a secured loan. Assets like real estate or machinery can be signed on as collateral if you default on your payments, making lenders more likely to approve your request. So, if you have valuable assets, then your business is more likely to be approved for larger financing amounts.

Assets can be particularly important if your business does not perform well on other credit metrics. If you have a high-value asset to use as collateral, then lenders are more likely to overlook bad marks on your credit. However, if you do use assets as collateral, then you should take care to ensure that you will be able to make payments on your loan or risk losing the assets.

Financial Health

Lenders also consider the overall financial health of your business when determining loan eligibility. They will want to look at financial statements, such as your cash flow statement, as well as your debt-to-income ratio.

Simply put, lenders want to see that your business is stable and solid. Income and cash flow statements will demonstrate that your business is generating more money than it spends, and they will show whether you can afford your monthly payment.

One of the most important metrics of financial health that lenders examine is your debt-to-income ratio. To get this number, you can divide your monthly payment obligations by your total income. A healthy business should have a low debt-to-income ratio, which should never exceed 36. If your debt-to-income ratio is low, then you will have an easier time securing funding.

READ MORE: Can You Get Equipment Financing with Bad Credit?

If you need essential equipment to expand your business and are unsure whether you qualify for a loan, talk to the experts at Global Leasing & Financial Services (GFLS). We can help you look more closely at the factors that determine your eligibility and provide guidance for improving your creditworthiness. GFLS is known for providing equipment financing to a wide range of credit tiers, using our internal GFRS funds, bank lines and non-bank providers. We work hard to earn our customers’ trust by providing top-quality products and best-in-class service. That’s why “when other lenders say no, we often say yes.”

Effective immediately Pat Chaffey has been chartered with the entire AACFB program responsibilities for Global Financial & Leasing Services. His Team members include Julian Sirull, Chuck Dale and Cathy Steadman. All future inquiries from members of the AACFB should be directed to

Effective immediately Pat Chaffey has been chartered with the entire AACFB program responsibilities for Global Financial & Leasing Services. His Team members include Julian Sirull, Chuck Dale and Cathy Steadman. All future inquiries from members of the AACFB should be directed to

When financing major business equipment purchases, choosing the right lender from the many out there can boggle the mind. Shady companies and scam artists have flourished in the age of the internet, and sometimes, it can seem hard to tell who’s legitimate and who isn’t.

When financing major business equipment purchases, choosing the right lender from the many out there can boggle the mind. Shady companies and scam artists have flourished in the age of the internet, and sometimes, it can seem hard to tell who’s legitimate and who isn’t.

The Difference Between the Essentials and Nice-to-Haves

The Difference Between the Essentials and Nice-to-Haves

Communication is Key

Communication is Key

October marks the start of the 4th quarter and the beginning of the end of the tax year for many business owners. If you’ve been considering making purchases for your business, this might be the right time to buy. Your business benefits from having the goods or services available now, and your expense write offs can reduce your tax liability for this year.

October marks the start of the 4th quarter and the beginning of the end of the tax year for many business owners. If you’ve been considering making purchases for your business, this might be the right time to buy. Your business benefits from having the goods or services available now, and your expense write offs can reduce your tax liability for this year.

Prior to the global pandemic, the national unemployment rate was low, leaving millions of jobs unfilled. COVID-19 struck and unemployment soared, but with economic activity resuming, the unemployment rate fell to 7.9% in September.

Prior to the global pandemic, the national unemployment rate was low, leaving millions of jobs unfilled. COVID-19 struck and unemployment soared, but with economic activity resuming, the unemployment rate fell to 7.9% in September.